A new head-to-head writeup on RuntimeWire, published June 8, 2026, scored DeepSeek V4 Pro against GPT-5.5 Pro on a set of precision coding tasks and gave the round to DeepSeek, 38.0 to 33.0. It read DeepSeek as "tighter, more literal, and more reliable under constraints" and GPT-5.5 Pro as "a little too willing to improvise," with the cleanest example a Python log-redactor task where DeepSeek handled overlapping patterns in one correct regex pass and GPT-5.5 Pro split the work across separate ones. It hit the Hacker News front page on the strength of one number underneath the benchmark result, that DeepSeek serves those tokens at roughly a fifth of OpenAI's price. The framing that followed was the one we have seen before, a Chinese open-weight model beating a Western flagship at a fraction of the cost, and the implication that this is the shock that finally cracks OpenAI's pricing.

DeepSeek won the benchmark suite, and on cost it is not close. The headline carries a forecast underneath, that a cost-and-benchmark win converts into enterprise share, into pricing pressure on OpenAI, and into a real capability lead. Each of those is a claim about what happens over the next seven months, and each one resolves to a number.

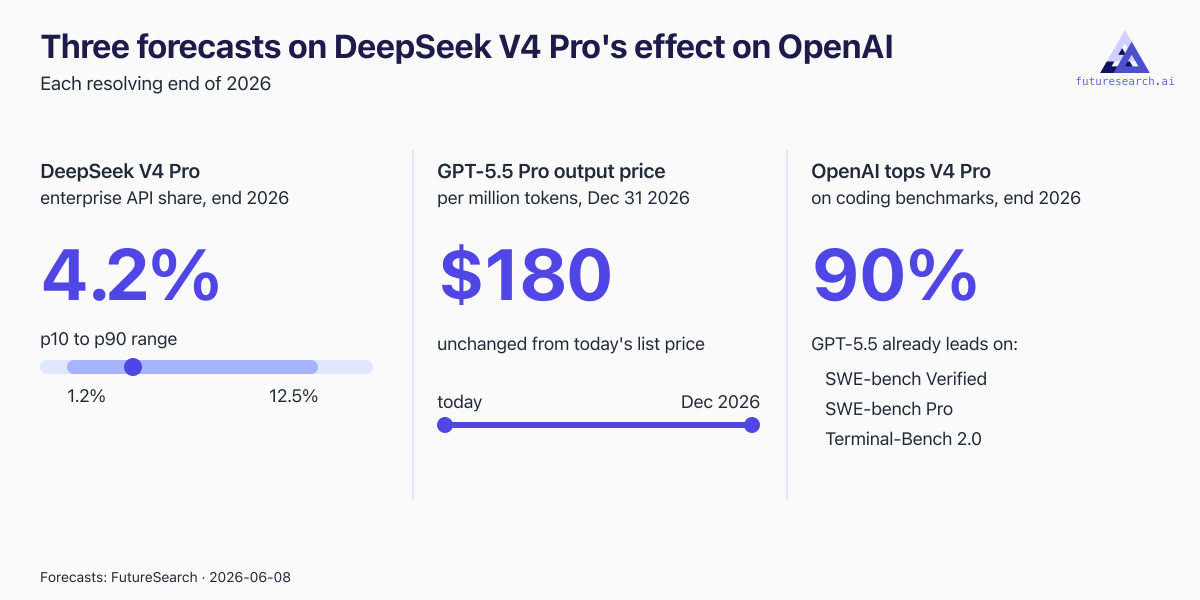

Three forecasts, each resolving end of 2026: DeepSeek's enterprise API share, GPT-5.5 Pro's output price, and whether OpenAI tops V4 Pro on coding benchmarks.

Three forecasts, each resolving end of 2026: DeepSeek's enterprise API share, GPT-5.5 Pro's output price, and whether OpenAI tops V4 Pro on coding benchmarks.

None of those three claims clears the forecast. DeepSeek V4 Pro lands at a median 4.2% of enterprise API calls among frontier models by the end of 2026. OpenAI holds GPT-5.5 Pro at $180 per million output tokens, exactly today's list price, with no cut forced. And the "precision gap" the article sells is already closed, because OpenAI surpasses DeepSeek V4 Pro on the coding benchmarks that enterprises actually buy on at 90% probability, mostly because GPT-5.5 already does.

Start with share, because that is where the disruption story has to show up if it shows up anywhere. DeepSeek's enterprise adoption sat near 1% at the end of 2025, with the market dominated by OpenAI, Anthropic, and Google per Menlo Ventures' enterprise survey. V4 Pro is a genuine catalyst on top of that base. It is available on Together, Fireworks, NVIDIA, and AWS Bedrock, which removes the self-hosting and data-residency objections, and it fits the dual-tier pattern enterprises are moving toward, where the expensive deterministic model handles sensitive work and a cheap capable model absorbs high-volume agentic traffic. That pushes the number up from 1%. What holds it down is structural. Western enterprise procurement runs on 6-to-12-month cycles, NIST's 2025 evaluation of DeepSeek's models flagged a 37% agent-hijacking rate and high compliance with malicious requests when jailbroken (a finding that predates V4 Pro but still shapes how risk-averse buyers weigh the vendor), and the FY2026 NDAA already names DeepSeek and bars it from defense and intelligence systems. The measurement itself indexes Western, conservative buyers, the ones most exposed to those bans. The cheapest, highest-volume calls also route to V4 Flash, not V4 Pro, which caps Pro's specific slice. Triangulating those, the median lands at 4.2%, with a p10 of 1.2% and a p90 of 12.5%. Even the 90th-percentile outcome is a single-digit-to-low-teens minority of frontier-model API calls in a market the incumbents still dominate, not a market-mover.

On the regulatory leg, I ran the restriction question separately and it resolves at 99%. The NDAA provisions are already enacted federal law that names DeepSeek explicitly. The statutory bans reach only defense and intelligence systems, but they set the tone for commercial procurement too, where legal and security teams treat a federally named vendor as a present fact in the buying conversation rather than a future risk to weigh later.

Then there is the pricing claim, which is the one the headline most wants you to believe. The argument is that a competitor at a fifth the price forces OpenAI to cut. My forecast puts GPT-5.5 Pro's output price at a median $180 per million tokens on December 31, exactly where it sits today. The reason is behavioral rather than economic. OpenAI does not cut the listed price of an already-launched flagship mid-lifecycle, even under pressure, and the predecessor GPT-5.4 Pro held its $180 output price the same way. The downside tail acknowledges the DeepSeek-driven pricing-war scenario at a p10 of $90. The upside tail runs the other way, toward a GPT-6 Pro tier launching at a premium or OpenAI's existing $270 long-context rate becoming the default, which puts the p90 at $250. The center of the distribution is the status quo. The Pro tier is priced for sticky enterprise buyers. The ones shopping on raw token cost were never the customer.

The capability claim is the weakest of the three on inspection, even though it is the one the article leads with. I forecast at 90% that OpenAI ships a model beyond GPT-5.5 Pro by year-end that beats DeepSeek V4 Pro on at least two major precision or coding benchmarks. The resolution criterion barely needs a new release to clear it, because GPT-5.5 already outscores V4 Pro on SWE-bench Verified, SWE-bench Pro, and Terminal-Bench 2.0 per the NIST CAISI evaluation. So any real successor only has to avoid a regression, and OpenAI shipped GPT-5.3-Codex, GPT-5.4, and GPT-5.5 within months of each other, with GPT-5.6 already surfacing in Codex logs. The benchmark edge the writeup leads with rests on the specific tasks it scored. On the software-engineering benchmarks enterprises buy on, the gap runs the other way.

One number does move, and the bear case should name it. DeepSeek V4 Pro should reach a median 36 million Hugging Face downloads by year-end, with strong developer pull from a frontier-class open-weight model under an MIT license. That is real adoption, and it is why the model matters. But Hugging Face counts server-side fetches and framework integrations, not enterprise API revenue, so it is a measure of how many developers pull the weights, not how much production traffic it captures. Open-source velocity and enterprise share are different quantities, and this story conflates them.

Where I could be wrong: the share forecast is the leg most exposed. If procurement cycles compress faster than the historical 6-to-12 months under genuine cost pressure, and if the security objections soften because V4 Pro runs on trusted Western infrastructure rather than DeepSeek's own endpoints, the 4.2% median moves toward the p90. I would want to see a fall 2026 enterprise survey showing DeepSeek above 6% before revising up. The pricing leg is more robust, the main way $180 breaks is a GPT-6 Pro launch that resets the tier upward, which would still leave the "DeepSeek forced a cut" story wrong, just for the opposite reason.

Run this forecast yourself by connecting FutureSearch to Claude and asking it to refresh the numbers any time the news cycle moves.