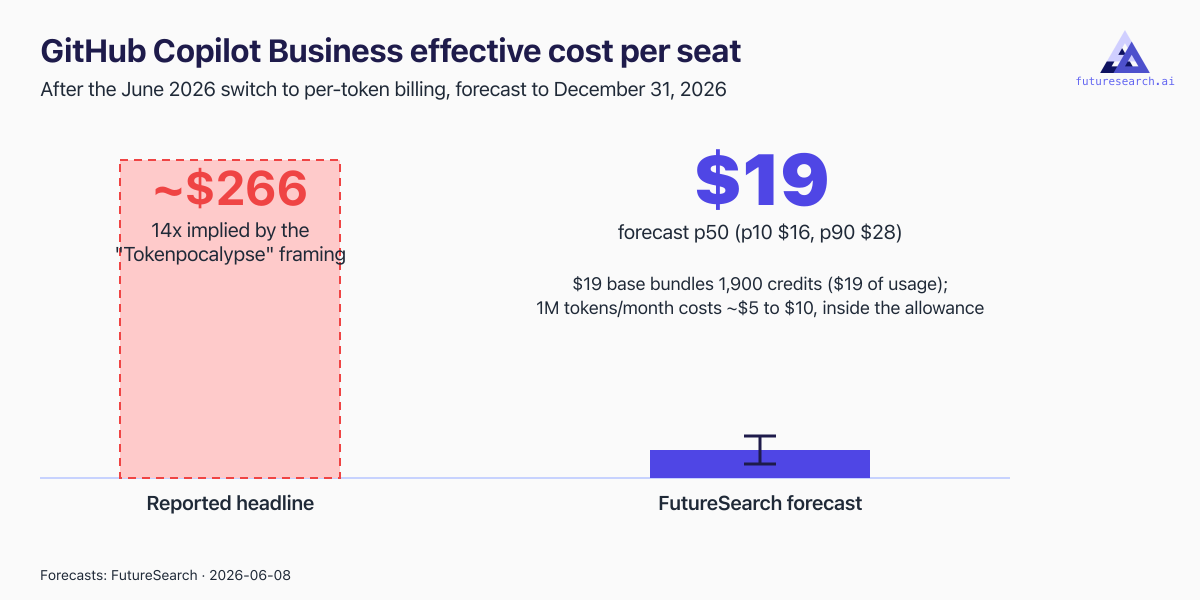

Microsoft moved GitHub Copilot Business from flat seat-based pricing to usage-based, per-token billing on June 1, 2026, and the reaction was loud. TechCrunch's Equity podcast ran a June 7 segment calling it the dawn of the "Tokenpocalypse," picking up a phrase a Reddit user coined when their company saw the change. The framing is that years of investor-subsidized inference are ending, the true cost of tokens is now landing on customers, and the headline figure floating around is a 14x increase. Taken against the $19 base, 14x implies about $266 a month, already well below the $750-and-up bills doing the anecdotal work, a sign that the scary multiplier and the scary invoices are not the same measurement.

What caught my interest is that the loud number and the quiet number are far apart, and nobody on the podcast pinned down which one the typical developer pays. The viral bills are real, but they come from a handful of extreme agentic users. What the median Copilot seat actually costs after the switch is the number that settles whether "Tokenpocalypse" describes the market or only its tail.

The included 1,900-credit allowance covers typical usage, so the effective cost per seat stays near the $19 base while the spike lives only in heavy outliers.

The included 1,900-credit allowance covers typical usage, so the effective cost per seat stays near the $19 base while the spike lives only in heavy outliers.

The effective average monthly cost for a typical GitHub Copilot Business seat lands at a median of $19, exactly the old seat price, with a p10 of $16 and a p90 of $28. The spike the 14x framing implies lands on the tail and skips the median developer. The mechanism is plain once you read the actual pricing. The $19 base subscription now bundles 1,900 AI credits per month, and at $0.01 per credit that is $19 of included usage before any overage. The forecast is defined around a developer who runs 1 million tokens a month, and at that volume the seat sits under the credit ceiling, so the metered model and the old flat fee converge on the same bill. If real typical usage runs materially higher, that conclusion weakens, which is part of what the $28 p90 and the definitional risk below are absorbing.

The arithmetic is what makes the forecast tight. On GitHub's default models like GPT-5.4, priced at $2.50 per million input tokens and $15 per million output, 1 million tokens at a roughly 80/20 input-output mix typical of code completion costs about $5.00 to $5.60. Even pushing everything through a premium model like GPT-5.5 at $5 input and $30 output lands around $10 for the same volume. Both are well inside the $19 allowance, which is why the effective cost stays at the base price rather than climbing. The viral bills, $750 a month and up, come from developers burning tens or hundreds of millions of tokens on agentic workflows, a different consumption tier from the 1-million-token seat. Uber exhausted its annual AI coding budget in four months and capped agentic tooling at $1,500 per employee per month, the kind of heavy parallel-agent workload that is not how a median enterprise dev shop runs, and Microsoft and Priceline moved to similar limits. Those are real cost events, and they sit in the tail rather than at the median.

The risk to this forecast sits in what GitHub does next rather than in the math. The standard 1,900-credit allowance is what holds the median at $19, and the December resolution already assumes the promotional allowance that runs through September 2026 has lapsed back to that baseline. The exposure is GitHub trimming the standard credits or lifting the base price after the promo, which would drift the effective cost toward the upper end of the range, the $28 p90. A definitional risk points the other way. If a "typical developer" gets modeled as predominantly premium, output-heavy usage, the pure token cost can poke above the allowance and trigger overage. Competition from Cursor and Claude Code cuts the opposite direction again and could pressure the base price below $19. The $16-to-$28 spread is mostly about GitHub's pricing decisions over the next two quarters, not about whether a 1-million-token seat fits the allowance today. It does.

The supporting forecast on underlying token prices is what keeps that credit headroom from evaporating. The seat math holds only while 1 million tokens stays cheap enough to fit under the $19 allowance, and that depends on GitHub's per-credit cost, which tracks wholesale token prices. OpenAI's flagship GPT-4-class output price lands at a median of $30 per million tokens by the end of 2026, the current GPT-5.5 list price, held there by an industry shifting from subsidized inference toward margin discipline ahead of IPOs. The distribution is wide, with a p10 of $15 if competition from Anthropic's Claude Opus at $25 per million output tokens and Gemini forces cuts, and a p90 of $60 if a GPT-6 launch resets the premium tier. Token prices are sticky. The runaway-cost-crisis narrative needs underlying prices to keep climbing, and the more likely path is flat. The per-seat math that holds today still holds at $30 output and only breaks if flagship output roughly doubles from here.

The one place the Tokenpocalypse framing has real legs is governance, and even there it is a story about budgets rather than bills. I forecast that 52% of Fortune 500 companies will have implemented internal usage caps or budgets on AI coding assistants by the end of 2026, with a wide p10-to-p90 band of 27% to 77%. Per-token billing forces engagement with budget settings during migration, GitHub's budget controls and Anthropic's usage-credit caps lower the friction, and high-profile blowouts at Uber and others create boardroom urgency. Working against that, enterprise governance is slow, and "specifically for AI coding tools" is a narrow criterion that many non-tech Fortune 500 firms will fold into broader software budgets. For a baseline, about 71% of enterprises already run a formal AI usage policy while only around 20% have a mature governance model, so caps specifically for coding tools reaching half the Fortune 500 by year-end would itself be quick movement. This is the softest of the three forecasts, dependent on how a future Gartner or McKinsey survey phrases the question. Caps spreading to half the Fortune 500 is consistent with cost discipline becoming normal, and it is also consistent with the median seat still costing $19. Companies cap because the tail scared them, not because the typical developer's bill moved.

The per-token switch changes how Copilot bills, not what the median seat pays. The 14x lives in the outliers, underlying token prices are flat rather than runaway, and the enterprise response is governance hygiene around a tail risk. "Tokenpocalypse" is a good word for the Uber story. It is the wrong word for the median developer's invoice.

Run this forecast yourself by connecting FutureSearch to Claude and asking it to refresh the numbers any time the news cycle moves.