At Computex on June 3, 2026, Intel filled in the details on Crescent Island, its next-generation data center inference GPU built on the Xe3P architecture. The headline design choice is that it skips HBM, the high-bandwidth memory that Nvidia and AMD accelerators depend on and that the whole industry is short on. Instead Crescent Island uses up to 480GB of LPDDR5X, the cheaper, more available commodity memory. Intel's pitch is an air-cooled, 350W PCIe card that drops into existing servers, dodges the HBM bottleneck, and gives cost-conscious clouds a way to run inference without paying the Nvidia tax.

The framing across the coverage is that this is Intel's credible shot at Nvidia and AMD in the data center. That is a forward-looking claim, and there is no consensus answer yet, because the chip has not shipped and no cloud has committed to it. The question I care about is not what Crescent Island is, but whether anyone who matters will buy it.

That's a forecasting question, so I forecast it.

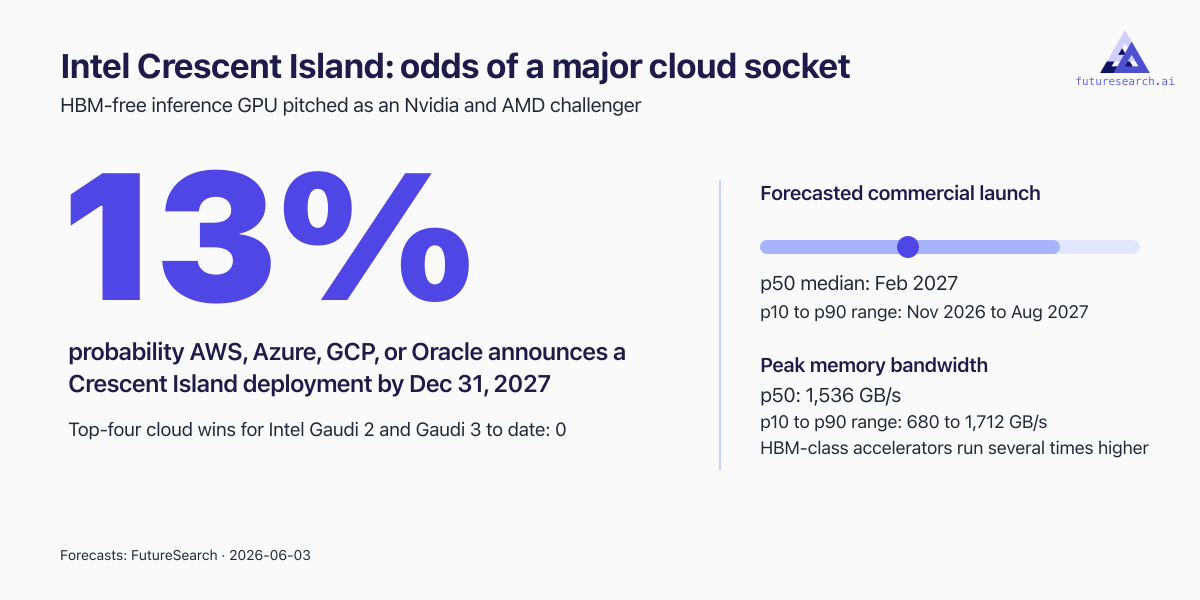

The 13% bar is the probability any of AWS, Azure, GCP, or Oracle announces a Crescent Island deployment by the end of 2027; the side panel shows the forecasted launch date and contested memory bandwidth.

The 13% bar is the probability any of AWS, Azure, GCP, or Oracle announces a Crescent Island deployment by the end of 2027; the side panel shows the forecasted launch date and contested memory bandwidth.

My conclusion is that the commercial story is mostly over before it starts. I put a 13% probability on any of the top-four clouds, AWS, Azure, Google Cloud, or Oracle, announcing a Crescent Island deployment by December 31, 2027. The chip that headlines call an Nvidia rival has, on my forecast, almost no path to a flagship cloud socket on the timeline that matters.

The core question is whether at least one major hyperscaler announces a Crescent Island deployment by the end of 2027, and 13% is a low number for a reason. Intel has run this play before and lost it. AWS deployed the original Gaudi 1 back in 2021, but none of the four major clouds picked up Gaudi 2 or Gaudi 3; Gaudi 3 missed even its modest revenue targets and got written off as a failure on immature software. The structural reasons that killed Gaudi are all still in place. Nvidia's CUDA ecosystem remains the moat, and Intel's oneAPI stack is far less adopted than either CUDA or ROCm. Worse for Intel, the four hyperscalers are not sitting around waiting for a third-party inference chip; they are pouring capital into their own custom silicon, AWS Trainium, Google TPUs, and Microsoft Maia. A cloud that has spent years building its own inference accelerator has very little reason to spend engineering time validating Intel's. As of today there are zero announced hyperscaler partnerships for the chip.

The timeline makes it worse, and that is where my launch-date forecast comes in. Intel has touted a second-half 2026 launch, and the article reads that as a year-end target. I think it slips. My median for commercial availability is mid-February 2027, with a p10 to p90 window running from November 2026 to August 2027. Intel's own customer sampling only starts in the second half of 2026, and the typical gap between sampling and general availability for a complex data center GPU is three to nine months. Intel also has a long history of slipping these dates; Ponte Vecchio was repeatedly delayed and Falcon Shores was canceled outright. If general availability lands in early 2027, a hyperscaler then has roughly twelve to eighteen months to validate the hardware, build out the software stack, and ship instances before the end of 2027. That is a brutally compressed window for cloud-scale deployment, and it leaves almost no margin for the kind of integration hiccup that Intel's products tend to produce. Skipping HBM solves a supply problem, but it does nothing about the integration runway, and the runway is the binding constraint.

Even the headline spec is contested, which is the third piece I forecast. A lot of the early coverage cited roughly 684 GB/s of memory bandwidth, the figure you get from assuming a 640-bit bus across 32-bit LPDDR5X packages. I think that number is wrong. My median is 1,536 GB/s, the figure that follows from a 1,280-bit bus across 64-bit packages running at 9600 MT/s, which is what the more technical leakers with access to PCB schematics are reporting and which matches the 64-bit LPDDR5X Intel already uses in Lunar Lake. My p10 to p90 spans 680 to 1,712 GB/s, so the distribution is bimodal, but I lean hard toward the high case because a sub-700 GB/s data center inference card would have the memory bandwidth of a consumer gaming GPU, which would undermine the entire reason to build it. Even the high case has a downside for Intel. At my median of 1,536 GB/s, Crescent Island still sits well below HBM-class accelerators, which run several times higher. The memory choice that makes the chip cheap and available is the same choice that caps its ceiling.

The single forecast I would watch for being wrong is the hyperscaler one, and the path to 13% being too low runs through Oracle. Oracle has been the most willing of the four to adopt non-Nvidia accelerators to win price-sensitive workloads, and a budget inference tier built on a cheap, air-cooled, high-capacity card is exactly the kind of bet Oracle has made before. A deep co-engineering partnership announced at a big event like re:Invent or the OCP Summit could also bypass the slow validation pipeline I am assuming, and Intel has not yet released compute benchmarks; if independent testing shows unprecedented cost-per-token efficiency, hyperscaler interest could move fast. So if I see Intel disclose strong, independently verified inference economics in late 2026, or any named cloud co-engineering commitment, I would raise the 13%. Absent that, the base rate of zero top-four wins across two Gaudi generations is the anchor I trust most.

If you'd like to try this forecast yourself, you can run our team-of-forecasters approach in futuresearch.ai/app. Just ask it to predict the probability that AWS, Azure, Google Cloud, or Oracle announces a deployment of Intel's Crescent Island GPU by the end of 2027. You can also connect FutureSearch to Claude and ask Claude to run it for you.