A June 2026 update of our April forecast, rewritten for the post-IPO market. The original article is preserved in full below.

At about $192 a share, near $2.5 trillion, SpaceX trades at roughly twice my estimate of its fair value. My sum-of-the-parts puts the business near $1.25 trillion, with Starlink, xAI, and Starship the largest pieces. The rest of the price is a scarcity premium from the IPO, and as the lock-ups expire and the float expands fourteenfold I expect it to deflate, pulling the stock toward $137 by mid-2027.

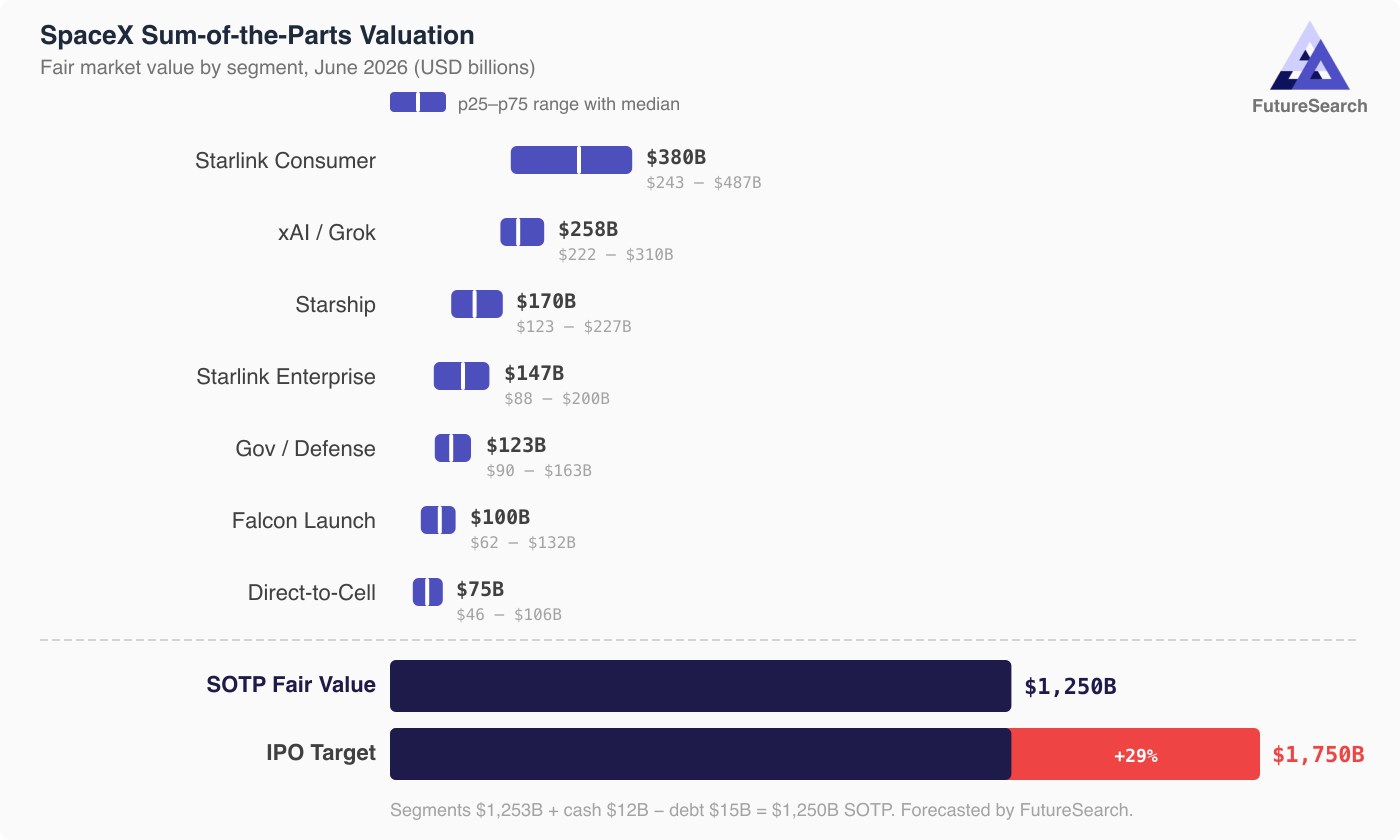

Our April sum-of-the-parts, the seven segments summing to $1.25 trillion, against today's $2.5 trillion market price.

When I called this IPO overpriced in April, I forecast a $158 day-one close; it closed at $160.95, and I grade that call below. The offering is settled now. The live question is the gap between price and value, and how it closes. That is a forecasting question, so I forecast it.

What SpaceX is worth

The chart above is my April sum-of-the-parts, seven segments valued as standalone businesses and summed to a fair value near $1.25 trillion, about $96 a share. That work is preserved in full below. Morningstar's discounted cash flow lands lower, near $780 billion, about $60 a share (Morningstar). Both sit far under the $2.5 trillion the market pays.

SpaceX's total 2026 revenue comes in at a median near $24 billion, up from about $18.7 billion in 2025, with a fat right tail to $33 billion that is almost entirely about whether the giant third-party compute contracts get recognized this year. Starlink stays the engine at roughly $15 to $17 billion, though average revenue per user has already slipped from $86 to $66 a month as growth moves into more price-sensitive markets (CNBC).

Under a strict reading, Grok plus Cursor as products, I forecast the AI segment near $9.9 billion of combined annualized revenue by year-end. Cursor exits around $6 to $6.5 billion, its growth decelerating as its share of the AI-coding market falls from about 41% to 26% with Anthropic taking roughly half the category (Forbes). Grok lands around $3 to $3.5 billion, carrying 117 million monthly users but only a 1.6% paid-conversion rate (Fortune). That sits right on the $10 billion line.

The filings define the segment more broadly, bundling legacy X advertising and, the part that matters, data-center leases. The Anthropic contract alone is reported at $1.25 billion a month, about $15 billion a year (TechCrunch), with another roughly $920 million a month from Google (CNBC). Counted that way, the AI segment clears $10 billion on the compute leases alone. So when the bull case rests $258 billion of value on the AI segment, the question to ask first is whether that is an AI product business or a landlord renting GPUs (Forbes). Those are different companies trading inside one ticker.

In the first quarter of 2026 SpaceX generated about $1 billion of operating cash against $10.1 billion of capital spending, roughly negative $9 billion of free cash flow in a single quarter, with AI buildout accounting for about three-quarters of the capex (SEC filing). Goldman Sachs does not model the company turning free-cash-flow positive until 2031 (Reuters). A business burning $9 billion a quarter to grow is worth a good deal less than one already throwing off cash, and that is most of the distance between $1.25 trillion and $2.5 trillion.

What $2.5 trillion requires

To pay $2.5 trillion, you have to believe everything goes right at once, the 75th percentile across every segment rather than the sum of independent medians. That was the core of the original article, and I turned it into a forecast. I defined four milestones that together make up the bull case, forecast each one, then forecast the joint outcome.

The four bull-case milestones and the probability of each: Starlink reaching 15 million subscribers (94%), a Starship operational orbital mission (74%), the AI segment reaching $10 billion (40%), and positive free cash flow (8%). All four must hold to justify the price.

At least one of the four lands with 98% probability, at least two with 84%, at least three with 48%, and all four with under 10%. So three of the four good things happening is close to a coin flip, and the whole drop from there to the full bull case is one milestone, free cash flow.

The capital spending required to hit the AI-revenue milestone and to fly Starship at the needed cadence is the same spending that drives the $9 billion quarterly burn from the last section. The two engines of the growth story are the thing preventing the profitability story. I estimated the joint probability three ways, multiplying the standalone odds, asking for the conjunction directly, and reading it off the how-many-land curve. They span roughly 2% to 10%, almost all of the disagreement about the cash-flow milestone, and I anchor to the low end. Today's price requires a low-probability sweep across every segment at once.

Why it trades above value

The original article bet the gap between price and value would converge over quarters, not days. In the first five trading days the stock did the opposite, running from $161 to about $192 as the gap widened, from roughly 29% below the offer to roughly 50% below the price. That looks like a strike against the thesis. It is the thesis.

At the IPO only about 4% of the company floated, and MSCI's early index-inclusion rules forced price-insensitive passive buying into that tiny float the day after listing. The dislocation is a supply problem, running on mechanics the business cannot change, and those mechanics unwind on a set calendar:

- Around August 2026. Near the first quarterly report, about 20% of locked shares release two trading days after earnings, with a conditional further 10% tranche if the stock has held 30% above the $135 offer, meaning above $175.50 (Yahoo Finance). This is the first real test of how much of the price is float scarcity.

- Around November 2026. The first audited earnings report, alongside another large tranche. Fundamentals and supply arrive together.

- December 8, 2026. The 180-day lock-up expires. By this point the tradable float has expanded from about 4% to as much as 58%, roughly fourteenfold (Business Insider).

- June 12 to 13, 2027. Musk's roughly 42% stake comes off its 366-day lock-up, the single largest block, landing just before my one-year mark.

Musk's block stays locked until next summer, which removes the largest seller for most of the window, and as the float grows passive funds have to keep buying to hold their index weights. S&P 500 inclusion would add a wall of demand, but it is blocked, because the index requires GAAP profitability and SpaceX is deeply unprofitable, with a $4.9 billion net loss in 2025. Net of all of it, the scarcity premium still bleeds off through each unlock.

SpaceX's tradable float over the lock-up calendar, from about 4% at the IPO to roughly 58% by the December expiry.

Where that leaves the stock

The business is worth about $1.25 trillion. The price is held above that by a float squeeze that unwinds on a known calendar, and the bull case that would justify the price is under 10%. So the stock should drift down toward value as the float normalizes, without reaching it, because a real Musk-and-AI premium survives the scarcity premium.

I put numbers on it at four points tied to the events that move a newly public stock, the supply shocks on the calendar rather than round-number dates. The medians trace a steady glide, roughly $192 today to $161, then $147, then $139, then $137 a year out.

Forecast price path for SPCX at four dates on the lock-up calendar. Median in indigo, candles span the 10th to 90th percentile.

The median never reaches fair value. A $137 median is about $1.8 trillion, still above my $1.25 trillion sum-of-the-parts and well above the $780 billion DCF. To touch fundamentals you go into the left tail, where the mid-2027 25th percentile of $97 lands on the sum-of-the-parts number and the 10th percentile of $66 sits on the DCF. The distributions are wide, $66 to $281 a year out, so the median is a center of mass, not a target, and there is a live upside tail in which index flows and AI exuberance carry the stock back to new highs. I placed the one-year reading just after Musk's shares unlock in June 2027, so it captures the moment of peak supply.

Everything here is dated and gradable. The live questions are the August unlock and the first earnings, whether Starship returns to flight and reaches an operational orbital mission, where Starlink subscribers and ARPU land at year-end, what the first audited statements say about the cash burn, and how the stock absorbs the December lock-up and Musk's June 2027 unlock. I will grade each against its resolution date as it arrives, and update this page when I do.

I ran these forecasts on June 18, 2026. Every question carries explicit resolution criteria and a resolution date.

Run this SpaceX forecast yourself, free →

How the original call scored

The day-one price call was a hit. I forecast a median day-one close of $158, a 17% pop. SPCX closed its first session at $160.95, up 19%, an error under 2%. I will keep the caveat I made at the time. This was not a sharp call that beat the market. The Hyperliquid pre-IPO perpetual had already converged to about $157 by June 10 (CoinDesk), so the best market signal and my model landed in the same place. I matched the best available number. I did not beat it.

The fair-value thesis is not gradable yet, and it is running against me in the short term. The bet was that price converges toward my roughly $1.25 trillion estimate over quarters, not days. It has been days, so there is no verdict, and in the near term the stock moved the wrong way, the price-to-value gap widening from about 29% to about 50% as the scarcity premium inflated. The forward forecast above is my updated account of where that thesis stands. I still think the premium deflates as the float normalizes through 2026 and 2027, but I now model the mechanism with dates rather than asserting it, and even my median no longer expects a full reversion to fair value inside a year.

The original article, preserved

Published April 1, 2026, last updated June 11, 2026, the day before trading began. Preserved as written.

A $1.75 Trillion IPO Would Be Overpaying 30% for SpaceX

A forecast of the fair market value of SpaceX's businesses as it IPOs at $135 per share, roughly $1.77 trillion, on June 12, 2026

SpaceX has priced the largest IPO in history at a fixed $135 per share, roughly $1.77 trillion, with trading set to begin June 12 (Nasdaq: SPCX). Our sum-of-the-parts forecast puts SpaceX's median fair value near $1.25 trillion, about 29% below that price.

SpaceX filed confidentially for an IPO on April 1, 2026, flipped its S-1 public on May 20, and set a fixed $135 price with no bookbuild range, an unusual structure for any IPO and unprecedented at this size. Order books closed June 10 at roughly 4x oversubscribed, with more than $250 billion in orders against the $75 billion raise.

I found this valuation interesting because SpaceX is a conglomerate now, so valuing the business segments together has a lot of intangible value. But my particular interest was because the IPO will happen in June (or later), so the question is not: what is SpaceX worth now, but what will SpaceX be worth then?

That's a forecasting question, so I decided to forecast it.

I broke SpaceX into seven business segments and forecast what the fair market value of each will be as of June 2026, assuming the IPO happens then. My conclusion is that for the company to be fairly valued at $1.75 trillion in June, each of its businesses would need to outperform between now and then.

Red on IPO bar shows the 29% premium over median forecasted fair value.

Red on IPO bar shows the 29% premium over median forecasted fair value.

At median forecasted values: Starlink Consumer Broadband at $380B (9.2M subscribers, ~38x revenue), xAI/Grok at $258B (anchored by the $250B merger), Starship Commercial Launch at $170B (pre-revenue option value), Starlink Enterprise/Maritime/Aviation at $147B, Government/Defense at $123B (~$22B contract backlog), Falcon 9/Heavy at $100B (~60-70% of global launches), and Starlink Direct-to-Cell at $75B (backed by $17-19B in EchoStar spectrum).

This totals $1,253B. Adding $11.6B in cash and liquid assets, subtracting ~$15B in total debt (SpaceX standalone obligations, remaining xAI inherited debt, EchoStar spectrum commitments), the sum-of-the-parts equity value is approximately $1,250 billion, 29% below the $1.75 trillion IPO target.

Run this SpaceX forecast yourself, free →

Where does the $500 billion gap come from? The SOTP method sums forecasted medians, but the IPO prices correlated upside, as if all businesses are valued more in my 75th percentile forecast. If investors are bullish on Starlink, they're simultaneously bullish on Starship, xAI, and defense. Taking the 75th percentile across all segments instead of the 50th brings the total to ~$1,675B, close to the target. The $1.75T price is "everything goes right" pricing.

SpaceX may also be one of the rare conglomerate premium cases. Conglomerates usually trade at a discount because investors prefer pure-play exposure. But the narrative that Starlink + Starship + xAI creates something no single segment could (orbital data centers, AI-powered global connectivity) may justify paying above the sum of parts. And the largest IPO in history will generate extraordinary retail demand: an up-to-30% retail allocation versus the typical 5-10%.

The gray market spent the run-up moving toward this page's number, though it has a long way to go. The most active pre-IPO market, the Hyperliquid SPCX perpetual, slid from about $216 in mid-May to about $157 on June 10, cutting the implied first-day pop from 60% to roughly 16%. That still prices SpaceX near $2.06 trillion. Our own price forecast, run the night before trading, lands in the same place: a median day-one close of $158, a 17% pop. To be clear, these are two different quantities: $158 is a prediction of what the stock will trade at on day one, and $1.25 trillion is an estimate of what the business is worth. The bet underneath this article is that the first number converges toward the second over quarters, not days.

A few things stand out. Starlink in all three forms (consumer, enterprise, direct-to-cell) accounts for $602B, or 48% of segment value and 34% of the IPO price. A longer-term forecast of whether Starlink can grow from 9.2M subscribers to 50M+ while expanding revenue per user through enterprise, maritime, aviation, and direct-to-cell channels is critical. I anchored to what others are saying, but I'm skeptical.

The other area where I'm extremely skeptical is xAI at $258B, with ~$430M quarterly revenue against $1.46B quarterly losses, valued almost entirely on the merger anchor from four months earlier. I've forecasted previously that I'd need to see more evidence that xAI is a frontier lab before believing it could be worth this much.

Starship at $170B is pure option value on technology still in advanced testing. And the physical assets (satellites, launch pads, factories, the Falcon fleet) are worth roughly $46B at fair market value, 2.6% of the IPO price. Nobody is buying SpaceX for its factories.

Finally, I should say the fair market value really is just what people are willing to pay. Perhaps the intangibles are worth a 30% pop, that wouldn't be that unusual in IPOs. But based on my forecasts of value, it's not worth it unless everything goes really well all together for them. Trading begins June 12, and I'll grade this forecast against the close.

Want to reproduce this result? Here's the starter prompt to use:

Break SpaceX into its major business segments and forecast the fair market value of each one in billions USD, as of the planned June 2026 IPO. Treat each segment as if it were a standalone company. Then sum the medians, add cash, subtract debt, and compare to the rumored $1.75 trillion IPO target.

Or, if you'd prefer a step-by-step walkthrough (including help adding FutureSearch to Claude Code), then see the SpaceX valuation guide.

See also: Forecasts of Anthropic and OpenAI's IPO dates and post-IPO valuations

Run this forecast yourself by connecting FutureSearch to Claude and asking it to refresh the numbers as the lock-up calendar plays out.